Entering clinical rotations is an exhilarating milestone in your nursing career, but it also marks the moment your professional liability shifts from theoretical to tangible. While your university may provide basic coverage, relying solely on institutional policies can leave significant gaps in your protection. This student nurse practitioner malpractice insurance guide is designed to navigate the complexities of liability, ensuring your future career remains shielded from the unpredictable nature of healthcare litigation.

Understanding the Critical Need for Student Nurse Practitioner Malpractice Insurance

The transition from a registered nurse to a provider role involves a heightened level of clinical decision-making and autonomy. Even under supervision, a simple diagnostic error or charting omission can lead to devastating legal consequences for a student. Investing in student nurse practitioner malpractice insurance ensures that you have a dedicated legal defense team focused solely on your interests, rather than the university’s bottom line.

Why University-Provided Coverage Often Falls Short for NP Students

- Shared Policy Limits: * Institutional policies often have an aggregate limit shared among all students in a cohort.

- If multiple students are named in a single lawsuit, the funds may be exhausted before your individual defense is settled.

- You have no control over the legal strategy or whether the school chooses to settle just to save costs.

- Lack of Personal License Protection: * Most school policies protect the university’s assets, not your individual RN license.

- If a patient files a complaint with the Board of Nursing, the school policy rarely pays for your legal counsel.

- Protecting your license is vital because a disciplinary action can end your career before it begins.

- Geographic and Activity Gaps: * School coverage typically only applies to hours logged for specific course credit.

- It may not cover volunteer work, health fairs, or shadowing hours not explicitly required by the syllabus.

The Financial Reality of Medical Malpractice in Advanced Practice

- Legal Defense Costs: * Even if you are eventually found not liable, the cost of expert witnesses and attorney hours is staggering.

- Out-of-pocket legal fees for a simple malpractice deposition can exceed $5,000 per day.

- Settlement Payouts: * Advanced practice students are held to a higher standard of care than undergraduate students.

- Settlements in primary care or acute care NP roles often reach six or seven figures depending on long-term patient disability.

- Future Insurability Issues: * A gap in coverage or a history of an uninsured claim can result in massive premiums once you graduate.

- Carrying your own policy creates a “clean” insurance history that demonstrates professional responsibility.

Are you struggling with complex nursing clinicals? Our PhD-level editors at StudentResearch.net provide expert guidance on advanced practice assignments. Ensure your papers meet rigorous UK and US academic standards with our specialized nursing editorial support. Let our experts help you succeed today!

Navigating Policy Types: Occurrence vs. Claims-Made Coverage

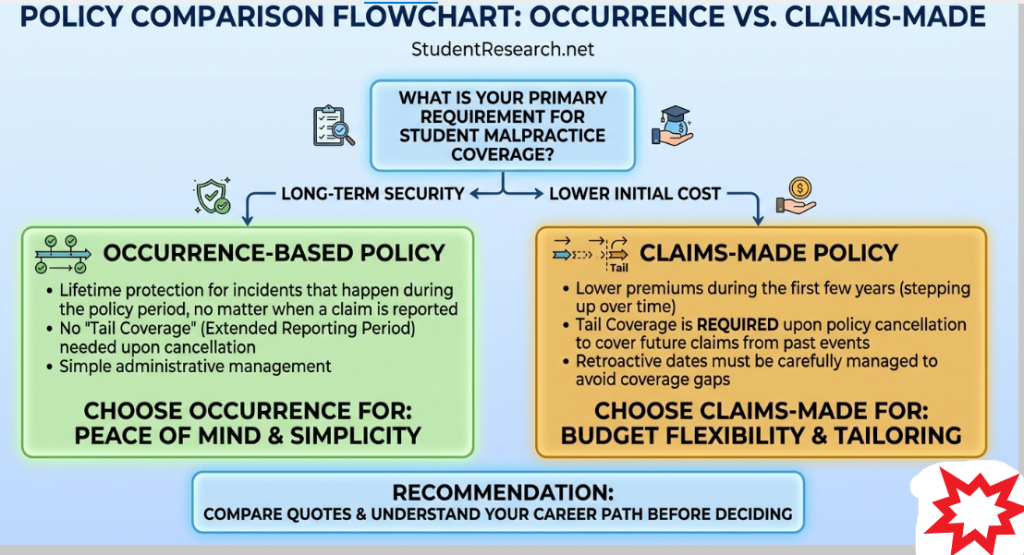

Choosing the right policy structure is the most technical aspect of securing student nurse practitioner malpractice insurance. You must decide between a policy that covers incidents based on when they happened versus when the claim is filed. Understanding these nuances is vital for long-term security, especially since lawsuits can be filed years after a clinical rotation ends.

Determining the Benefits of Occurrence-Based Policies

- Lifetime Coverage for the Period: * An occurrence policy covers you for any incident that happened while the policy was active.

- It does not matter if the claim is filed five years after you graduate and the policy is canceled.

- This is the “gold standard” for students because it offers permanent protection for that specific timeframe.

- No “Tail” Insurance Necessary: * You do not need to purchase additional reporting period coverage when you move into your first professional role.

- This saves you thousands of dollars in transition costs between school and career.

- Simple Administrative Management: * You don’t have to worry about “retroactive dates” or maintaining a continuous link with one company.

Analyzing the Mechanics of Claims-Made Policies

- Initial Premium Savings: * These policies start with very low rates that “step up” in price over a five-year period.

- For a student on a tight budget, the initial low cost can be attractive, but it carries future obligations.

- The Tail Coverage Requirement: * If you cancel a claims-made policy without buying a “tail,” you lose all coverage for the time you were in school.

- Tail coverage usually costs 200% of your annual premium, making it a significant end-of-program expense.

- The Retroactive Date Trap: * If you switch from one claims-made provider to another, you must ensure the new policy “picks up” your old start date.

- Failing to sync these dates leaves a “gap” where you have zero protection for past clinical mistakes.

Key Features to Look for in an NP Student Liability Policy

Not all student nurse practitioner malpractice insurance policies are created equal, and the “cheapest” option often lacks essential riders. When reviewing your declarations page, look for specific monetary limits and supplemental coverages that protect your professional reputation. Prioritizing comprehensive features now prevents out-of-pocket expenses later.

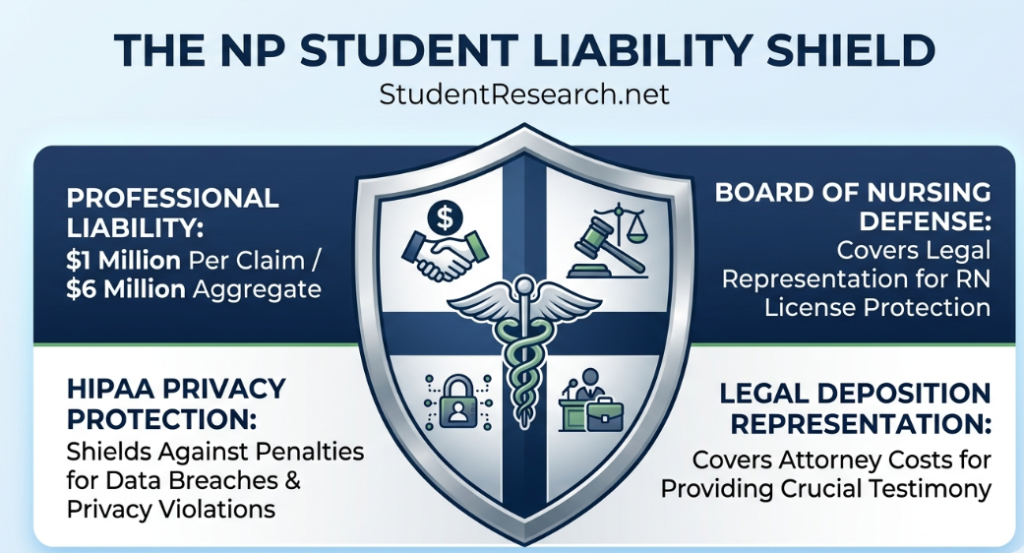

Essential Coverage Limits and Supplemental Benefits

- Standard $1 Million/$6 Million Limits: * $1 Million is the maximum the insurer pays for a single claim.

- $6 Million (or $3 Million) is the annual aggregate for all claims combined.

- These limits are often required by major hospital systems like the Mayo Clinic or HCA.

- Board of Nursing (BON) Defense: * Covers legal fees if a patient complains to the board about your ethics or clinical competence.

- This is separate from a malpractice lawsuit and handles the administrative side of your license.

- First Aid and Lost Wages Reimbursement: * Reimburses you for expenses incurred if you provide emergency aid outside of school hours.

- Pays you a daily rate (often $250-$500) for time missed from work to attend court or depositions.

Comparison of Leading Insurance Providers for NP Students

| Provider Name | Policy Structure | Annual Student Rate | Key Differentiator |

|---|---|---|---|

| NSO (Nursing Service Organization) | Occurrence | $35 – $50 | Portable coverage follows you to any clinical site |

| Berxi (Berkshire Hathaway) | Occurrence | $40 – $60 | Direct-to-consumer model with fast digital claims |

| CM&F Group | Occurrence | $38 – $55 | 24/7 legal advice hotline for policyholders |

| Proliability (Mercer) | Occurrence | $45 – $65 | Partnership with major nursing associations |

The Role of Student Research in Risk Management

Engagement in student research is a hallmark of Doctor of Nursing Practice (DNP) and Master’s programs, often involving data collection from real patient populations. While research is academic, any intervention or data breach during the study can lead to liability claims. Ensuring your student nurse practitioner malpractice insurance covers your “academic and research pursuits” is a non-negotiable step for the modern scholar.

Protecting Your Academic and Clinical Investigations

- Informed Consent Liability: * Risks associated with failing to properly document participant consent during student research.

- If a participant feels coerced or misled during a study, they can sue the student investigator directly.

- Insurance provides the legal backing to prove that IRB protocols were followed meticulously.

- HIPAA and Data Privacy: * Research often involves handling sensitive Protected Health Information (PHI).

- A lost laptop or a hacked cloud drive containing research data can trigger massive HIPAA fines.

- Liability policies often include a “Cyber Security” rider to handle the costs of patient notification and credit monitoring.

- Intellectual Property and Plagiarism Defense: * While rare, some policies offer protection against claims of academic theft or data manipulation.

- Having insurance ensures that a dispute over student research authorship doesn’t drain your personal savings.

How Evidence-Based Practice Reduces Malpractice Risk

- Standard of Care Alignment: * Using the latest student research allows you to justify your clinical actions in court.

- If you can prove your treatment plan was based on current literature, it is much harder for a plaintiff to prove negligence.

- Protocol-Based Safety: * Research-backed checklists reduce the likelihood of “never events” like wrong-site procedures.

- Following validated screening tools (like the PHQ-9 for depression) provides a structured defense of your assessment.

- Documentation as Defense: * Literature shows that detailed, objective charting is the #1 defense against malpractice.

- Learning the “do’s and don’ts” of charting through student research helps you avoid common pitfalls.

Common Clinical Scenarios Where Insurance is Vital

Real-world clinical environments are fast-paced, and as a student, you are often navigating new Electronic Health Record (EHR) systems and unfamiliar protocols. Student nurse practitioner malpractice insurance acts as a safety net when the “ideal” classroom scenario meets the “chaotic” reality of the clinic. Understanding where errors most frequently occur allows you to be more vigilant during your rotations.

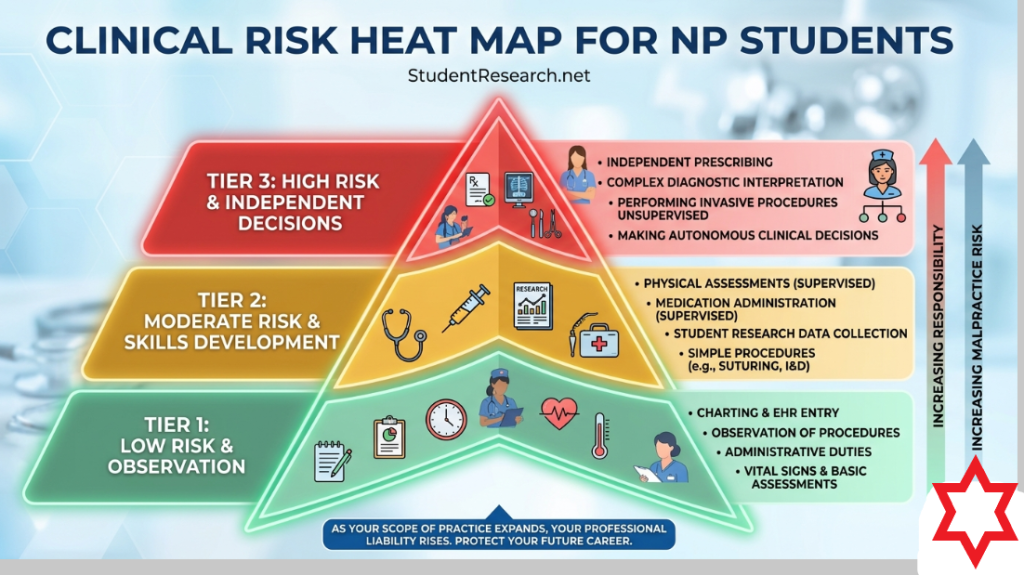

High-Risk Errors in the Advanced Practice Student Role

- Medication and Prescribing Errors: * H4: Incorrect Dosing and Calculations: Miscalculating a pediatric dose or a geriatric renal adjustment.

- H4: Interaction Oversight: Failing to notice a contraindication between a new script and the patient’s herbal supplements.

- H4: Transcription Errors: Entering the wrong frequency or route into the EHR under a preceptor’s login.

- Diagnostic and Monitoring Failures: * H4: Misinterpretation of Lab Results: Missing an elevated potassium level or a critical troponin rise.

- H4: Delayed Referrals: Failing to flag a suspicious skin lesion that later turns out to be malignant melanoma.

- H4: Incomplete Physical Exams: Omitting a neurological check that would have caught an early-stage stroke.

Issues with Supervision and Scope of Practice

- The “Solo” Student Pitfall: * Performing a procedure (like an I&D or suturing) without the preceptor in the room.

- If a complication arises while you are unsupervised, you are highly vulnerable to a “negligence per se” claim.

- Miscommunication of Status: * Failing to notify the attending provider of a significant change in a patient’s vitals.

- If the patient decompensates, the “failure to rescue” claim will include everyone in the chain of command, including the student.

- Scope Creep: * Administering a type of care or medication that is outside the NP student handbook guidelines.

- Insurance is your only defense if a facility tries to blame you for an outcome they should have supervised.

Step-by-Step Guide to Purchasing Your Policy

Buying student nurse practitioner malpractice insurance is a straightforward process that can usually be completed online in under ten minutes. However, the timing of your purchase is critical to ensure there are no gaps between your classroom learning and your first day at a clinical site. Follow these sequential steps to ensure you are fully protected before you ever touch a patient.

Strategic Timeline for Coverage Acquisition

- Step 1: Audit Your Program Requirements: * Review your university’s Clinical Placement Agreement.

- Some state laws require specific “minimum” coverage amounts that differ from school policies.

- Step 2: Compare Three Mainstream Providers: * Use the T-column table above to look at NSO, Berxi, and CM&F.

- Look specifically for the “Board Defense” dollar amount, as this varies widely between $10k and $25k.

- Step 3: Complete the Online Application: * You will need your current RN license number and the date you expect to graduate.

- Be honest about any previous clinical incidents or board actions on your RN license.

Managing Your Policy Post-Purchase

- Download and Save Your Certificate of Insurance (COI): * Hospitals will not allow you on the floor without a current COI on file.

- Keep a copy on your phone or in a cloud folder (like Google Drive) for instant access during site visits.

- Set an Annual Renewal Reminder: * Student policies usually expire after 12 months; do not let it lapse during your final semester.

- A gap of even one day can be problematic if an incident occurred during that window.

- Notify the Insurer of Program Changes: * If you switch from a Family NP to a Psychiatric NP track, update your insurer.

- Different specialties may have slightly different risk profiles or premium rates.

Conclusion: Securing Your Future in Advanced Practice

Securing student nurse practitioner malpractice insurance is more than just a clinical requirement; it is a fundamental act of professional self-care. By understanding policy types, leveraging insights from student research, and choosing a robust policy, you are building a fortress around your hard-earned nursing license. As you move forward, remember that being an empowered provider starts with being a protected student. Obtain student nurse practitioner malpractice insurance to shield your clinical journey and secure your professional future with total confidence.

Meta Description: Obtain student nurse practitioner malpractice insurance to shield your clinical journey and secure your professional future with total confidence.

Ready to elevate your academic performance? StudentResearch.net offers comprehensive support for DNP and MSN projects, ensuring your work reflects professional excellence. Don’t let tight deadlines hinder your career goals; click here to order your custom academic outline now!